Local-for-Local Manufacturing is Driving Reshoring Opportunities

The advantage of being closer to demand is the ability to shorten lead times and to fulfill customer needs faster and more effectively.

(MH&L — Pierfrancesco Manenti: 4-29-16) There are no patriotic reasons behind the ongoing wave of reshoring, although many politicians are trying to navigate this wave today. The reason why so many companies—including Apple, Ford, Caterpillar, General Electric, Intel and others—have reshored some production plants back to their home country is primarily because they wanted to be closer to their customers. The increase in labor cost in traditional low-cost countries like China, combined with the emergence of new automation technologies, is making reshoring a viable option today.

Changing Manufacturing Footprint Strategies

Over the past few years, the approach to manufacturing footprint strategies has changed dramatically. Companies are moving from a strategy essentially driven by low-cost labor arbitrage to one driven by the needs of improving customer fulfillment through more agility and responsiveness. More than half of SCM World’s community members tell us they are planning to reshore at least some of their production capacity.

One of our members—Under Armour, a U.S. supplier of sportswear and casual apparel—has recently unveiled its reshoring strategies aiming to manufacture apparel and footwear back in the United States. The company is currently staffing a new advanced manufacturing innovation facility near the company’s Baltimore corporate headquarters to investigate new production technologies and develop a new manufacturing model that would make this possible. Under Armour believes that “local-for-local manufacturing drives growth with better products and a more efficient supply chain.”

Bringing the labor-intensive apparel and footwear industry back to the U.S. is also at the top of Walmart’s agenda. Last January, the company’s U.S. Manufacturing Innovation Fund awarded $2.8 million to five universities for their ability to address two key barriers to increased domestic manufacturing: first, to reduce the cost of textile production, and second, to improve common manufacturing processes with broad application to many types of consumer products.

Walmart’s U.S. Manufacturing Innovation Fund was launched in 2013 as the company’s long-term strategy to help revitalize U.S. manufacturing through a commitment to buy an additional $250 billion in products that support U.S. jobs by 2023. Based on Walmart’s research and surveys of its customers, the company found that “Made in USA” is a strong driver of purchase decisions, second only to price. Products across all categories are, in fact, perceived to have higher quality if made in the U.S.

Local-for-Local Manufacturing

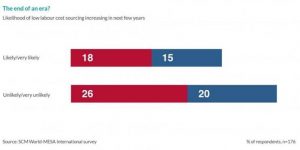

With the dramatic increase in labor costs in many traditional low-cost countries like China, the business case for pure low-cost country sourcing is less obvious today than it was previously. The majority of respondents to a SCM World survey consider it unlikely that their companies will increase sourcing from lower labor cost countries over the next few years. The share of these companies is 13 percentage points higher than those who say they are likely to increase offshoring.

With this development in mind, last year one of our community members from the CPG industry came to us asking, “Where is the next China?” This initial question quickly changed into a more strategic one: “How can we make a long-term, sustainable impact on our manufacturing footprint strategy?” To answer this question, the company entered a phase of profound transformation built on a multi-year roadmap geared around investing more in automation and hiring more highly-skilled people. The long-term strategy is to move manufacturing closer to demand, which doesn’t necessarily mean bringing manufacturing back to its home country.

Perhaps the best example of local-for-local manufacturing is from Danish toy maker Lego. Unlike most other firms in its industry, Lego did not race off to build low-cost production capacity in China. Bali Padda, Lego’s executive vice president and chief operating officer, describes Lego’s local-for-local manufacturing footprint as comprising regional production sites, serving the U.S. market from Monterrey, Mexico, and European markets from facilities in Denmark, the Czech Republic and Hungary. The company is now setting up in China to serve the Chinese domestic market.

“It is our strategy to have production close to our core markets in order to secure short lead-times and world-class service to our customers and consumers, and it has proven a successful strategy,” says Padda. “In addition, by placing a manufacturing site in the region we reduce our environmental impact as we will reduce the need for transporting products from Europe to be sold in Asia.” The way for Lego to maintain its core production close to markets —including its largest manufacturing plants in high-wage Denmark—is through leveraging cutting edge automation. If you can’t do low-cost labor arbitrage, then automate!

The Business Case for Reshoring

Modern manufacturers understand that there are several other factors they have to consider beyond low-labor-cost opportunities when adding new production capacity. For example: lead-time considerations, sustainability implications, higher working capital and supply chain disruptions—to name but a few—are essential drivers, which have often been overlooked in the past.

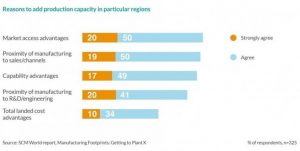

The SCM World community helps us again to identify the most compelling reasons driving today’s manufacturers to add production capacity in different global regions:

- Market access. Opening or moving a plant in a certain new location means overcoming trading barriers and working with local partners for easier market access. It also means a better understanding of local demand and customer preferences.

- Proximity to demand. The advantage of being closer to demand is the ability to shorten lead times and to fulfill customer needs faster and more effectively. It also enables manufacturers to customize and localize products efficiently.

- Capability. Moving from capacity to capability means developing a higher degree of production flexibility, which can be achieved through levels of automation and highly-skilled resources.

- Proximity to R&D. Better integrating manufacturing and R&D drives more effective and efficient new product introduction.

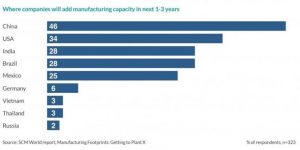

Local-for-local manufacturing is, therefore, the emerging manufacturing footprint strategy. For this reason, China continues to be a magnet for new manufacturing capacity. As shown in an SCM World report, China is the top country for manufacturers to add new capacity in the next few years. This is not happening because China is a low-cost country, but rather because China is one of world’s largest economies.

Is Reshoring Real?

Last December, two conflicting reports about reshoring trends were released. One by A.T. Kearney stated that reshoring may be over; the other by the Boston Consulting Group insisted that reshoring is alive and kicking. ATK’s authors report that “overall domestic U.S. manufacturing activity failed to keep pace with the import of offshore manufactured goods over the five-year period.” On the other hand, “31% of respondents to BCG’s fourth annual survey … said that their companies are most likely to add production capacity in the U.S. within five years for goods sold in the U.S., while 20% said they are most likely to add capacity in China.”

I think both are right! And wrong! As pointed out in this blog, “ATK tries to measure reshoring indirectly by measuring imports. […] BCG uses surveys of reshoring plans, but companies’ actions often differ from plans.” We should instead measure the hard facts. The opportunity comes from McKinsey’s Digital globalization: The new era of global flows report. They found that global consumption growth is outpacing trade growth for a number of finished manufactured goods, such as cars, pharmaceuticals and plastic goods. Where are those goods being made? Well, the answer is very likely to be found in local-for-local manufacturing.

The original confusion here is on the meaning of the term reshoring. We shouldn’t consider reshoring simply as bringing back manufacturing to a home country. That doesn’t make any business sense per se, unless the home country has a thriving economy. I believe local-for-local manufacturing is a more appropriate term to describe today’s manufacturing footprint strategies. This might call for reshoring to home countries or nearshoring opportunities. It might well still call for low-cost country sourcing. The reality is that companies will only add production capacity to a certain location if the economics makes sense.

As a matter of fact, manufacturing footprint design increasingly requires considering dozens of separate variables, each with unique variances and all interacting in ways that change with time. Time is especially critical to the analysis because factories exist in space and society in ways that affect people’s lives as well as return on invested capital.

The main conclusion, then, is that manufacturing footprint design demands the best strategic and technical thinking available. It is not a one-time activity, nor can be simplified down to formulae in a spreadsheet. Tackling this dynamically involves a number of elements that makes companies winners or losers.

(Pierfrancesco Manenti is VP of research at SCM World, a cross-industry learning community powered by influential supply chain practitioners.)